From greenqueen.com.hk

By Anay Mridul

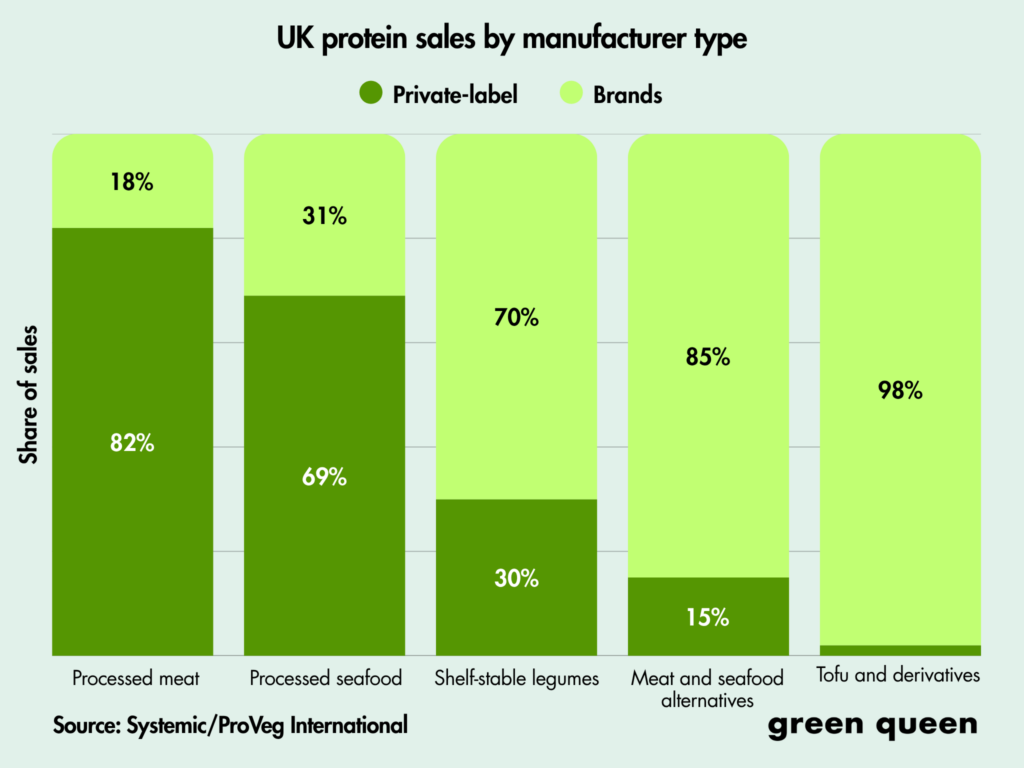

Private-label brands make up 82% of processed meat sales in the UK, but only 15% of plant-based alternatives – and retailers risk losing out on billions if they don’t promote protein diversification.

British supermarkets could stand to gain billions, make progress on their climate targets, and address the country’s fibre deficiency by championing plant-based proteins, shows a new report.

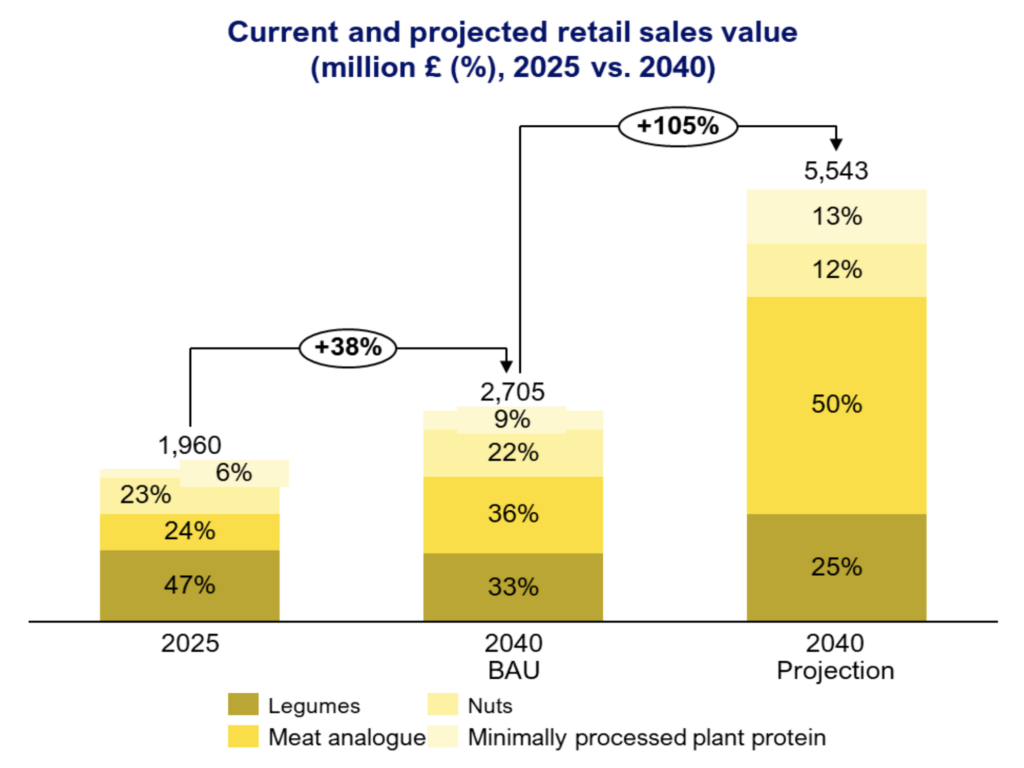

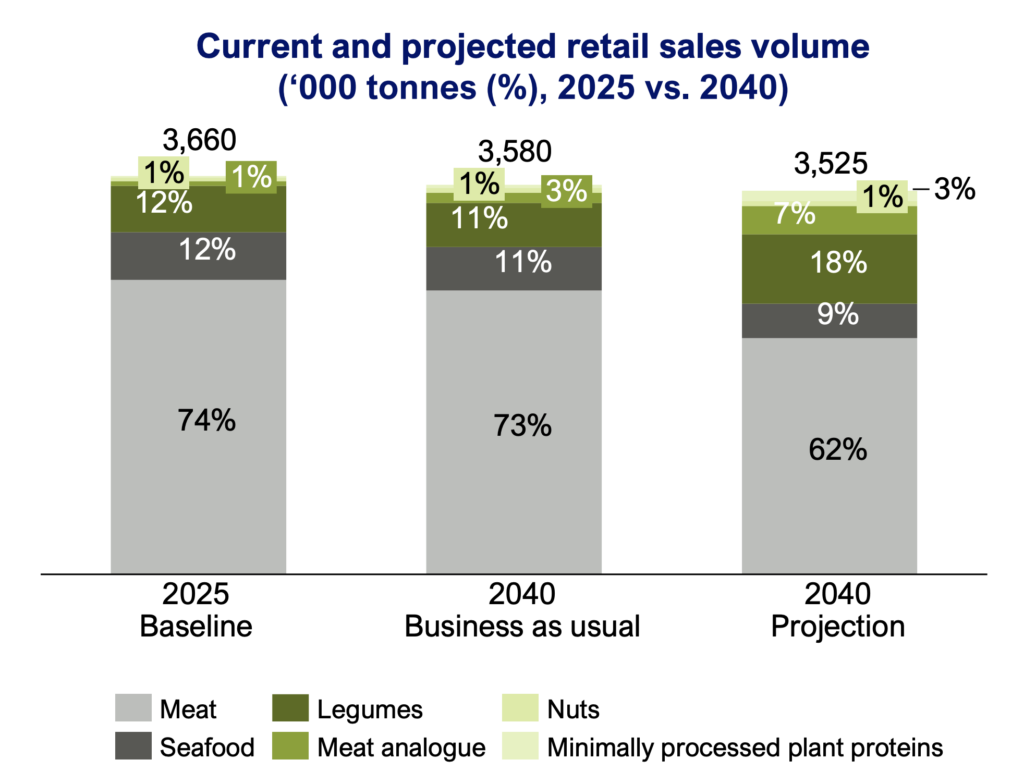

Analysis by Systemiq and ProVeg International reveals the share of protein sales from plant-based foods in the UK is set to double from 14% in 2025 to 29% in 2040.

The problem? Retailers are lagging. The research suggests that supermarkets’ own-label brands account for 85% of processed meat sales, but only 15% of plant-based meat and seafood sales, and just 2% of tofu and derivatives.

Closing this gap would give retailers direct control over pricing, margins, and category direction, which Systemiq says is the most effective way to capture the plant-based opportunity.

“The current protein model is exposed on cost, volatility, emissions and health. Are retailers ready to treat plant-based protein as a core business, rather than a peripheral experimentation?” Systemiq co-founder and managing director Jeremy Oppenheim wrote in a LinkedIn post.

Plant-based meat sees sales hike and approaches price parity

Following the highs of 2020-21 and the subsequent correction, the UK’s plant-based category is now recovering and maturing. For instance, Lidl blasted past its target to increase alternative meat and dairy sales by 400% by 2025, recording a 694% hike since 2020. And Tesco reported that the sector was “back in growth”, with sales of vegan mince up by nearly 25% and whole-food proteins by 12%.

Even with whole-food options dominating the landscape, meat and seafood alternatives are performing well, with retail sales growing by 5% between 2024 and 2025.

The vegan market’s expected growth until 2040 will primarily be driven by both sets of proteins: meat analogues and legumes. The former are set to approach price parity with processed meat by 2028 (some products reached that mark last year), and private-label expansion represents the largest commercial opportunity here.

Legumes, meanwhile, are already cheaper and have the greatest growth potential in absolute volumes – although consumer uptake is constrained by limited awareness, underscoring the need for convenience formats and own-brand expansion.

Minimally processed proteins like tofu are cost-competitive with (or cheaper than) meat, too – though they remain underleveraged in-store. And the consumption of nuts remains five times below recommended levels, and their growth lies in positioning beyond snacking into daily cooking.

“Plant-based proteins cost less per kilogram, so revenue per unit is lower than the animal-based equivalent. However, they also carry higher and more stable margins than meat and seafood, strengthening overall profitability,” the report states.

Under a business-as-usual scenario, plant-based food sales are forecast to grow by 38% over the next decade-and-a-half, totalling £2.7B. If supermarkets were to take charge on the protein diversification front, they could double this value, crossing £5.5B by 2040.

How retailers can seize the plant-based opportunity

The benefits of a plant-rich transition aren’t just financial. Systemiq’s analysis shows that protein diversification could reduce greenhouse gas emissions by 16%, land use by 14%, and water consumption by 13%, making it a key lever for retailers’ scope 3 emissions targets.

Moreover, this shift would drive a 71% intake in fibre compared to a business-as-usual scenario by 2040, closing around 11% of the UK’s current fibre gap, in addition to saving over £108M in associated public healthcare costs.

Systemic suggests that retailer action is the most directly controllable growth driver, underlining three key levers: increasing the share of private-label plant-based products, placing them alongside their animal-derived equivalents with clear value communication, and measuring ‘protein split’ sales to create a level playing field for vegan food.

Calls for protein diversification are growing across Europe – last week, 25 civil society groups urged supermarkets to measure, disclose, set targets and take action on the protein split, noting that 60% of their sales should come from plant-based sources.

Systemiq is asking retailers in the UK to start measuring the ratio of plant-to-animal food sales using a recognised and shared methodology (as their counterparts in the Netherlands are doing), and implement ambitious individual and sector-wide actions to rebalance sales towards plant-rich consumption, in line with the Eat-Lancet Commission‘s Planetary Health Diet.

In fact, industry-wide collaboration reduces first-mover risk and builds shared infrastructure. So the report suggests sharing pre-competitive best practices, using industry platforms to coordinate sector-wide action that outlasts singular initiatives, and engaging the government jointly to support plant-based protein policies, such as updated dietary guidelines and tax and subsidy reforms.

“The commercial case for protein diversification is stronger than most British retailers currently recognise,” said Brian Shaw, senior director at Systemiq.

“We have heard from multiple British retailers that there is no climate action without protein diversification, and our analysis validates that. For retailers serious about reaching net zero, rebalancing their protein portfolio is one of the most powerful levers available.”

No comments:

Post a Comment